If you’re nearing retirement or already enjoying it you’re probably asking one of the most important questions: Will my money last?

You’re not alone. Many retirees and pre-retirees share concerns about maintaining financial security throughout retirement, especially as people live longer and retirement can span decades. Market uncertainty, inflation, and unexpected expenses can all make it harder to feel confident about the future.

That’s why many people look for financial solutions designed to help protect their savings while providing opportunities for growth and reliable income. For some, annuities may play an important role in a retirement strategy.

How Financial Professionals Help Address Retirement Concerns

Financial professionals often help clients prepare for retirement by building diversified strategies designed to balance growth potential with protection from market volatility. Depending on a person’s goals, risk tolerance, and income needs, protective solutions such as Fixed Annuities and Fixed Index Annuities (FIAs) may be considered as part of an overall retirement plan.

These products are often used to help address common retirement risks, including:

Sequence of Returns Risk

The risk that poor market performance early in retirement could negatively impact how long retirement savings last.

Longevity Risk

The possibility of outliving your retirement savings.

The Role of Fixed and Fixed Index Annuities in a Retirement Plan

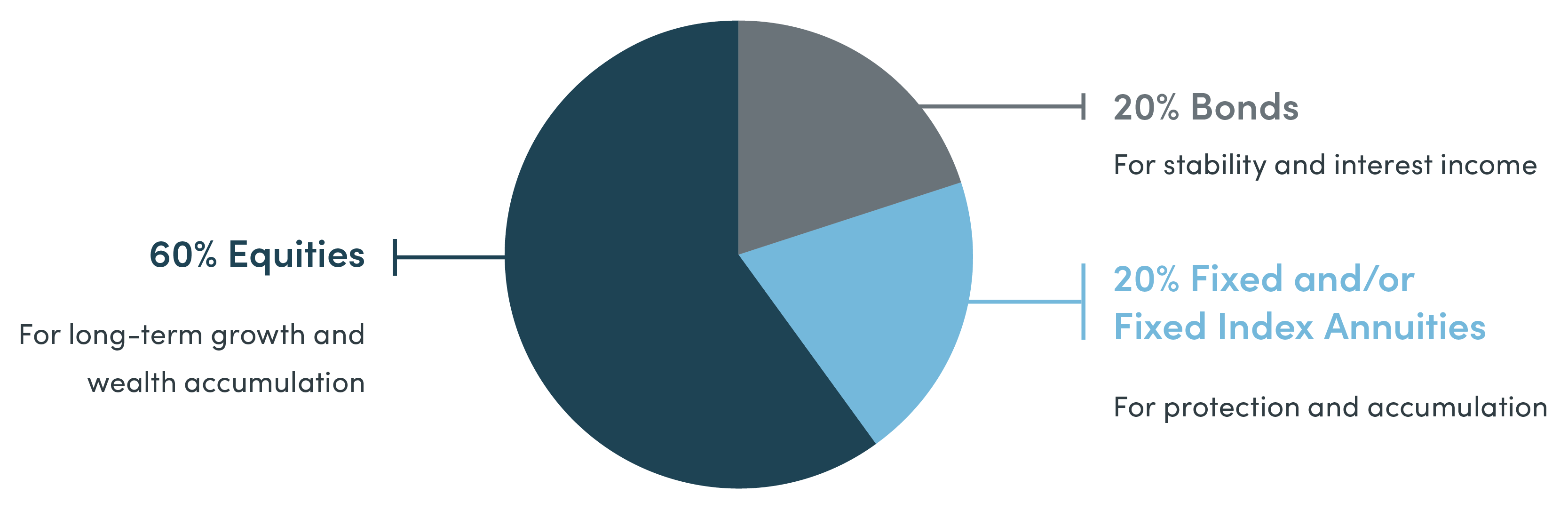

A well-diversified retirement portfolio helps balance accumulation potential, income stability, and at least some protection from risk. Traditionally, many retirees have relied on a mix of stocks and bonds, but in today’s environment of volatility and uncertainty, that may not be enough.

By incorporating a Fixed Annuity or an FIA into your retirement plan, you can de-risk a portion of your assets while choosing which accumulation options you’re most comfortable with.

Understanding the Difference

Fixed Annuities (Like MYGAs) - A Fixed Annuity, often structured as a Multi-Year Guaranteed Annuity (MYGA), lets you lock in a guaranteed interest rate for a set term, usually between 3 and 7 years.

Fixed Index Annuities (FIAs) - FIAs work a little differently. Instead of just offering a fixed interest rate, they give you the chance to potentially receive a higher interest rate based on part of the performance of a financial index (like the S&P 500®). But here’s the best part: you won’t lose your principal, even if the index value drops.

A Comparison: Fixed Annuities & Fixed Index Annuities

| Fixed Annuities | Fixed Index Annuities | |

| Guaranteed Interest Rate1 | ||

| Opportunity for higher interest than traditional fixed-income products | ||

| Potential for market-linked accumulation | ||

| Tax-deferred accumulation | ||

| Death benefit (avoids probate) | ||

| Principal protection (no market losses) | ||

| Access to a portion of your money, even during the surrender charge period |

Bringing It All Together

Planning for retirement goes beyond saving. It’s about protecting what you’ve built and making sure it lasts. Fixed and Fixed Index Annuities can provide stability while also offering accumulation potential to help support your long-term financial goals.

Both Fixed Annuities and Fixed Index Annuities are designed to provide protection at a time in life when you may not be able to afford significant market risk, but still want your money working for you.

- A Fixed Annuity offers a guaranteed interest rate and growth potential.

- A Fixed Index Annuity offers those same benefits, plus the potential to earn more based on index performance without market losses.

Both offer protection, flexibility, and the confidence that comes with knowing your money is working for you, not against you.

1Some FIAs offer guaranteed interest rates on certain strategies (e.g., fixed account or guaranteed rate options).